Last week, GourmetPro expert Jay Mota took us through the strategies employed by three global brands to successfully enter the Indian Indian. In case you missed it…

This week, GourmetPro expert Sanjeev Srivastav gives us the lowdown on today’s Indian consumer and what makes them tick. Sanjeev is a highly accomplished professional with over 30 years of experience in driving growth and operational efficiency in the F&B sector. He has a strong understanding of how Indian consumers are evolving and how to best meet them where they are.

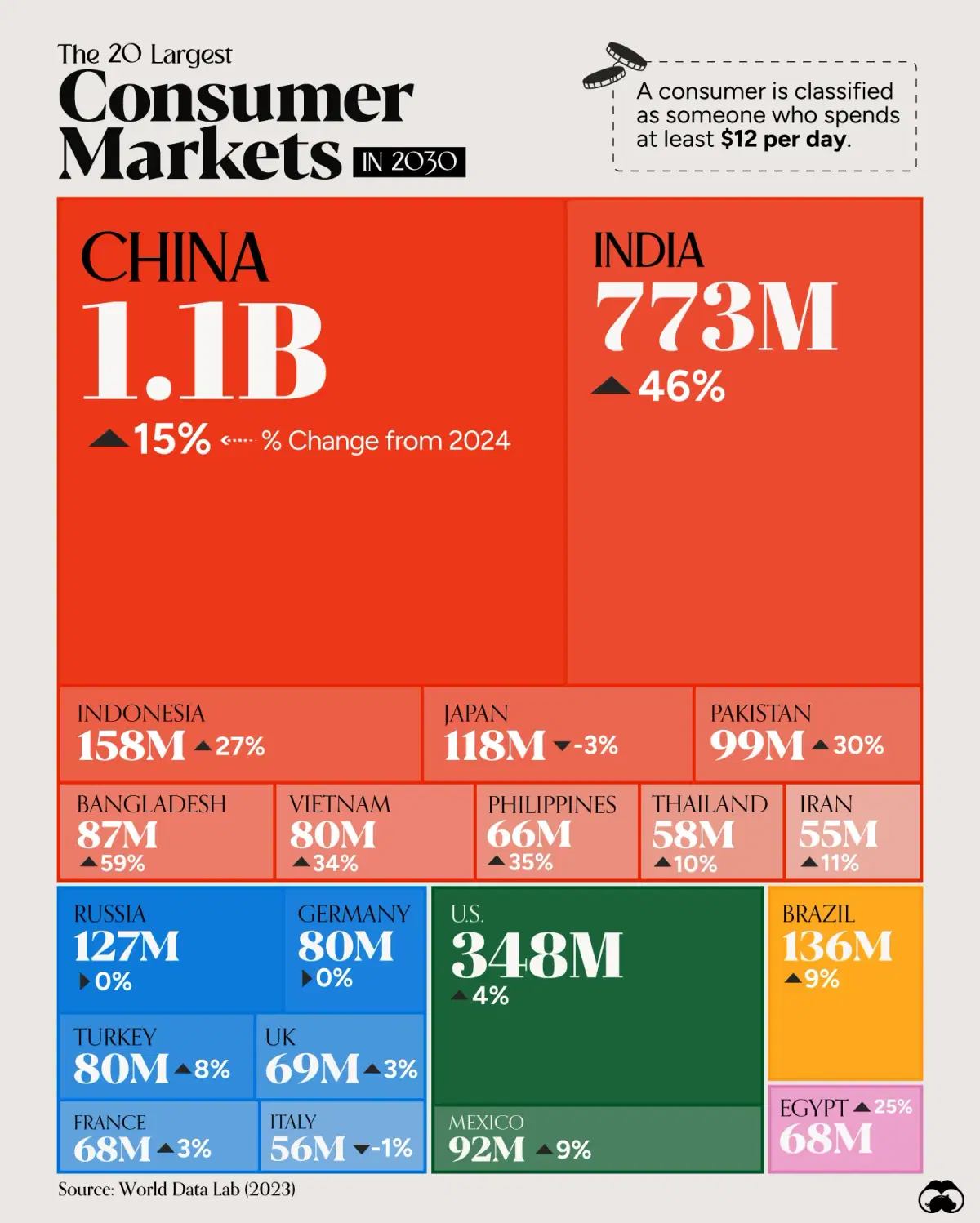

With a population of 1.45 billion people, India is one of the largest and most complex consumer markets in the world. By 2030, it is estimated to become the second largest consumer market after China, based on World Data Lab projections. The sheer size and diversity of India present immense opportunities for both domestic and global brands. However, understanding the nuances of this complex market is crucial for success.

Source: Visual Capitalist

Contrary to popular belief, Indian consumers have a strong propensity to spend – when they see value. While the market is vast, it’s segmented by language, culture, and income levels, meaning strategies must be adapted to each region and demographic. But before formulating these strategies, it’s vital to understand the consumers themselves. Let’s dive into the characteristics that define today’s Indian consumers and how brands can cater to their evolving preferences.

Value conscious, yet willing to pay for quality

Indian consumers are often perceived as price-sensitive, but they are increasingly willing to pay more when they perceive good value. Whether it’s for premium or daily essentials, they seek a strong price-to-value ratio. Brands introducing new products need to clearly differentiate their offerings in terms of quality, taste, and packaging to justify higher price points.

A case in point is the cheese market.

The top brand in this category in India has a national presence and a dominant market share. Competing against such a well-established brand is a challenge for any new entrant in the market. When a global brand entered the market in 2018, it was priced at a premium – almost 40% higher than the market leader.

The problem was further compounded by the fact that the Indian consumer cheese market was still at a very nascent stage. As of 2022, India’s annual per capita cheese consumption was less than 200 grams, compared to the global annual average of 7 kg.

To succeed, the global brand had to tailor its cheese to suit the Indian palate, which prefers milder flavors compared to traditional cheeses. This customization was essential in gaining acceptance, particularly among children, who became key consumers of the product.

Another strategy was offering the cheese in smaller, snack-sized portions. This approach not only aligned with Indian consumers' value-for-money expectations but also helped introduce the product as a convenient snack for children.

The packaging and portion control played a role in overcoming resistance to the premium price by positioning the product as both high-quality and practical.

Rising demand for convenience

India’s consumer landscape is shifting towards convenience-based shopping and product formats. There is a growing trend of moving away from loose, unpackaged foods toward safer, packaged options. Ready-to-cook and ready-to-eat foods are also gaining traction, especially as more households adopt busier lifestyles.

Convenience doesn’t just refer to product preparation – it also includes smaller portion sizes and single-serve packs, which cater to affordability and practicality.

According to Innova, there has been a net increase of 3% in convenience food usage globally over the last year. India in particular has seen remarkable growth, with 45% more consumers using more convenience food in the past 12 months. The growth was driven largely by younger consumers and higher-income groups. This shift towards convenience is particularly pronounced in urban areas, where consumers are willing to pay extra for quicker service and delivery.

E-commerce has played a significant role in this trend. During the pandemic, digital platforms enabled consumers to shop from home, a habit that has now become deeply embedded in both urban and rural populations. Quick and easy access to products, combined with the convenience of home delivery, has accelerated the growth of online shopping, further driving the demand for convenience foods.

India’s e-commerce market is currently valued at US$70 billion and is projected to reach US$325 billion by 2030. The quick commerce market grew at a significant 73% during 2023-24. It is currently worth US$3.34 billion, and is expected to reach US$9.95 billion by 2029. According to the NIQ Shopper Trends 2024, 31% of urban Indians now use quick commerce for their primary grocery shopping, while 39% use it for top-ups.

Don’t miss this chance to discover how upcycling is transforming food systems and creating value where others see waste.

Join us on 21 November 2024!

The impact of digitization

Over the last decade, India’s internet penetration has quadrupled. According to the Internet and Mobile Association of India, over 55% – or 820 million – of Indians were active internet users in 2023.

India’s rapid digital transformation has revolutionized consumer behavior. It has democratized access to information, allowing consumers to make more informed purchasing decisions. Digital platforms have also become a powerful tool for brands looking to reach consumers across India.

Digital platforms provide easy access to product reviews, comparisons, and detailed information, empowering consumers to make thoughtful choices. This is reshaping how consumers interact with brands and products. For businesses, the digital boom has opened new opportunities for reaching a wider audience and fostering engagement.

In fact, India has leapfrogged the traditional organized retail trajectory, going from unorganized/semi-organized retail directly to online shopping. While traditional retail remains the dominant channel for the grocery segment, it is undergoing significant structural changes, leading to better experiences for shoppers. India’s retail market structure is complex, but these changes are leading to its simplification and allowing for better access for new brands to reach end consumers.

Migration patterns have also played an important role here. A key example is India’s leading online grocer’s growth in Kolkata post-COVID. Many people who had migrated to other cities pre-COVID and came back home during the pandemic introduced digital shopping habits to their families. This helped the online grocer gain a foothold in conservative markets like Kolkata, where online shopping was previously less common.

The importance of regional preferences

India’s diversity extends beyond language and culture – it also includes distinct regional food preferences. To succeed, brands need to adapt their products to local tastes. A one-size-fits-all approach won’t work in such a fragmented market, where regional and local brands often outperform national players due to their understanding of local consumer preferences.

For example, in the spice market, Everest and MDH are national leaders, but the next biggest brand, Sakthi Masala, focuses primarily on a single state, Tamil Nadu. Sakthi’s success shows the importance of catering to specific regional preferences. Understanding local tastes and nuances is equally important for global brands entering the Indian market.

Source: Sakthi Masala

Some international companies have successfully navigated this by acquiring local brands. For instance, Norwegian conglomerate Orkla acquired MTR Foods and Eastern Condiments, both of which have a strong presence in South Indian cuisine. By leveraging local expertise, global brands can tap into regional consumer bases more effectively.

Like what you’re reading?

Openness to experimentation

While traditional tastes remain important, younger Indian consumers are increasingly open to experimenting with new flavors and products. This trend is more pronounced in urban areas, where the growing middle class is eager to try innovative food and beverage offerings. This interest is also driven by growing internet penetration, which has exposed Indian consumers to global flavors and formats.

For example, the popularity of Korean food has skyrocketed, with major instant noodle brands like Maggi, Knorr, and Top Ramen launching Korean variants. The market for Korean noodles in India grew from INR20 million in 2021 to over INR650 million by 2023, showcasing how rapidly consumer preferences can shift toward international trends.

Growing health consciousness

Health awareness is on the rise in India, with more consumers looking for products that not only taste good but also offer better nutritional value. As concerns about obesity, diabetes, and heart disease grow, the demand for healthier food options has surged.

According to a 2022 study by Avendus, India’s health food market is expected to reach US$30 billion by 2026, growing at a CAGR of 20%. Per capita spending on health foods is also projected to double during this period. This growth is being driven by Millennials, many of whom are adopting concepts like food as medicine and functional ingredients.

Despite the rising interest in better-for-you eating and snacking, the health food segment still accounts for only 11% of India’s total packaged food and beverage market. This leaves significant room for growth, especially when compared to the US, where health food penetration is 31%.

Sustainability

While sustainability isn’t yet a top concern for most Indian consumers, it is gaining traction, particularly among Gen Z. Younger consumers are becoming more conscious of the environmental impact of their purchases, and this trend is expected to grow in importance over the next decade. A recent PwC India survey of 1,000 Indians found that 60% of Indian consumers were choosing sustainable products. They also showed a willingness to pay 13.1% above the average price for such products.

But for now, sustainability is an emerging trend, but brands that focus on sustainable practices and messaging may find themselves well-positioned as consumer awareness increases in the coming years.

******

Indian consumers today are more open than ever to exploring new and exciting F&B products. With growing disposable income, increased digital access, and a younger population eager to experiment with new flavors and products, the Indian market presents immense opportunities for innovation across different consumer and product segments.

While traditional tastes still hold strong, the willingness to embrace novelty and healthier options makes India a dynamic landscape for brands. The market is still young and evolving, offering plenty of room for brands – both global and local – to establish themselves and capture the attention of these adventurous and value-conscious consumers.

Want to leverage Sanjeev’s expertise to

explore opportunities in India?

🔊 We want to hear from you! 🔊

Tell us what you thought about today’s topic, if there’s any topic you’d like us to cover, or just drop a line to say ‘hey’!

Just hit “reply” to this email. We read and answer all messages. 💌

That’s all folks

Thanks for reading today’s newsletter.

See you next week.

About Us: GourmetPro is a global network of elite food and beverage industry talents. We provide fractional hiring solutions, allowing international managing directors to scale and transform their local resources and teams with high flexibility and expertise in more than 30 countries. Explore our services.

Made with ❤️ by GourmetPro - your network of Food & Beverage experts, on demand.

💖 And if you think someone you know might be interested in this edition of Market Shake, feel free to simply forward this email or click the button below. 💖